1. What is the Electrical Protective Equipment Market Overview – definition, scope, and significance?

The Electrical Protective Equipment (EPE) market encompasses products designed to safeguard workers from electrical hazards such as shock, arc flash, and burns. The scope includes insulated tools, face and eye protection, respiratory protection, protective apparel, and head protection, which are deployed across diverse end‑user segments like manufacturing, construction, oil & gas, healthcare, and transportation. Its significance lies in the critical role EPE plays in occupational safety, regulatory compliance (e.g., OSHA, IEC 61482), and the prevention of costly injuries or downtime. As industries increasingly automate and electrify processes, demand for reliable protective gear accelerates, making the market a foundational component of workplace risk‑management strategies.

2. What are the key drivers, restraints, challenges, and opportunities in the Electrical Protective Equipment Market?

Key drivers include stricter safety regulations, heightened awareness of arc‑flash injuries, and the electrification of equipment in emerging economies. Growing construction activity and expanding oil & gas infrastructure further boost demand. Restraints stem from high upfront costs of premium‑grade equipment and price sensitivity in low‑margin sectors. Challenges involve maintaining compliance across varied regional standards and ensuring consistent product quality amid rapid technological change. Opportunities arise from the adoption of lightweight, ergonomically designed gear, integration of smart sensors to monitor exposure, and the untapped potential in developing markets where electrical safety programs are still maturing.

3. What are the current and emerging growth trends shaping the Electrical Protective Equipment Market?

Current trends feature a shift toward multifunctional equipment that combines insulation, impact resistance, and chemical protection, reducing the need for multiple gear items. Emerging trends include the incorporation of Internet‑of‑Things (IoT) sensors within helmets and gloves to provide real‑time voltage detection, and the use of advanced composite materials that improve durability while decreasing weight. Another notable trend is the increasing preference for modular systems, enabling users to customize protection levels based on specific tasks. These trends collectively enhance user comfort, safety performance, and overall adoption rates.

4. How has COVID‑19 impacted the Electrical Protective Equipment Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains, leading to temporary shortages of raw materials such as high‑performance polymers. Concurrently, lockdowns slowed construction and manufacturing activities, dampening short‑term demand. However, the heightened emphasis on worker health and safety accelerated procurement of comprehensive protective solutions once operations resumed. Recovery has been steady, supported by the resumption of infrastructure projects and a surge in electrical system upgrades aimed at improving energy efficiency. The market is now on a clear upward trajectory, aligning with its projected CAGR of 4.04%.

5. Who are the major competitors in the Electrical Protective Equipment Market and what is the state of market consolidation?

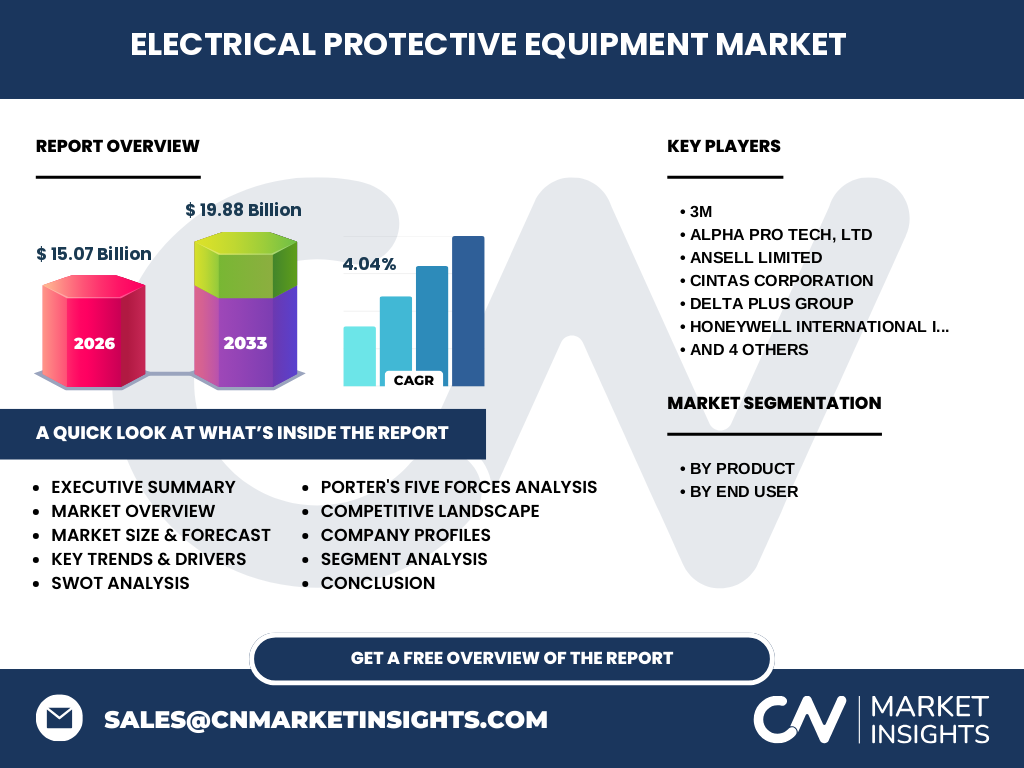

Leading competitors include 3M, ALPHA PRO TECH, Ltd, Ansell Limited, Cintas Corporation, Delta Plus Group, Honeywell International Inc., Lakeland Industries Inc., MSA Safety Incorporated, Mallcom (India) Limited, and NSA – National Safety Apparel. These firms differentiate through product innovation, global distribution networks, and strategic acquisitions. While the market remains fragmented, consolidation is evident as larger players acquire niche specialists to broaden their product portfolios and expand geographic reach, thereby strengthening their market positioning.

6. What are the high‑level insights and key findings presented in the Executive Summary?

The Executive Summary highlights a market valued at $15.07 billion in 2026, with a forecast reaching $19.88 billion by 2033, reflecting a 4.04% CAGR. Demand is propelled by regulatory pressure, electrification trends, and safety‑first corporate cultures. Insulated tools and protective apparel dominate the product mix, while manufacturing and construction are the largest end‑user segments. Regional analysis shows strong growth in North America and Asia‑Pacific, driven by infrastructure investments. Competitive dynamics point to ongoing consolidation, and innovation—particularly smart‑enabled gear—is identified as a primary growth lever.

7. What are the forecast expectations for the Electrical Protective Equipment Market from 2025 to 2032?

The market is projected to expand from its 2026 baseline of $15.07 billion to approximately $19.88 billion by 2033, maintaining an average annual growth rate of 4.04%. This steady expansion reflects continued regulatory enforcement, replacement cycles for aging equipment, and the rollout of new safety technologies. The forecast period anticipates increased adoption of integrated protection systems and a rise in demand from emerging economies undergoing rapid industrialization.

8. How is the Electrical Protective Equipment Market sized and shared by product and end‑user segmentation?

By product, the market is divided into insulated tools, face and eye protection, respiratory protection, protective apparels, and head protection. Each segment serves specific safety functions, with insulated tools and protective apparel representing the core of most safety programs. By end‑user, the market serves manufacturing, construction, oil & gas, healthcare, and transportation sectors. Manufacturing and construction together capture the largest share due to the high concentration of electrical work, while oil & gas and healthcare represent high‑growth niche segments where specialized protection is critical.

9. What is the geographic distribution of the Global Electrical Protective Equipment Market?

The global market is spread across key regions, including North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific monetary shares are not disclosed, North America leads in adoption due to rigorous safety legislation, whereas Asia‑Pacific is the fastest‑growing region, propelled by large‑scale infrastructure projects and expanding manufacturing bases.

10. What does the regional analysis reveal about market performance?

North America demonstrates robust performance, fueled by strict OSHA standards and replacement demand for aging protective gear. Europe follows closely, with EU directives driving compliance. Asia‑Pacific shows the strongest growth trajectory, underpinned by governmental initiatives to improve workplace safety and massive investments in construction and renewable energy. Latin America and the Middle East & Africa exhibit moderate growth, largely tied to regional oil & gas activities and emerging industrialization.

11. Which companies are leading in the Electrical Protective Equipment Market and what are their strategic approaches?

Industry leaders such as 3M and Honeywell leverage extensive R&D capabilities to introduce high‑performance, lightweight materials and sensor‑integrated solutions. Ansell focuses on ergonomic design and expands its global footprint through strategic partnerships. Delta Plus Group emphasizes regional customization, while MSA Safety prioritizes safety‑technology integration. These companies pursue strategies including product diversification, acquisitions of specialized firms, and expansion of distribution channels to capture broader market segments.

12. How does Porter’s Five Forces model apply to the Electrical Protective Equipment Market?

• Threat of new entrants: Moderate – high capital requirements and stringent certifications create barriers, but niche innovators can enter with specialized technology.

• Bargaining power of suppliers: Low to moderate – raw‑material suppliers are numerous, though high‑specification polymers can be limited.

• Bargaining power of buyers: Moderate – large industrial buyers negotiate volume discounts, yet safety compliance mandates minimum standards, reducing price‑only competition.

• Threat of substitutes: Low – alternatives that provide comparable electrical protection are scarce.

• Industry rivalry: High – many established players compete on innovation, price, and service, leading to ongoing product upgrades and strategic alliances.

13. What are the SWOT insights for the Electrical Protective Equipment Market?

Strengths: Critical safety function, regulatory backing, growing electrification.

Weaknesses: High product cost, dependence on raw‑material pricing, fragmented market.

Opportunities: Smart‑gear integration, expansion in developing economies, development of sustainable, recyclable materials.

Threats: Economic downturns affecting capital‑intensive sectors, potential regulatory changes that could shift compliance timelines, counterfeit products eroding brand trust.

14. How is value created and transferred in the Electrical Protective Equipment value chain?

The value chain begins with raw‑material suppliers (polymers, composites, electronic sensors), proceeds to design and engineering firms that develop safety‑certified products, then to manufacturers who produce and test the gear. Distribution follows via specialized safety distributors and direct sales to large end‑users. Aftermarket services—including inspection, refurbishment, and training—add value by ensuring long‑term compliance and fostering repeat business.

15. What investment insights should stakeholders consider when evaluating the Electrical Protective Equipment Market?

Investors should focus on companies with robust R&D pipelines for smart‑enabled protective gear, as these are poised for premium pricing and market differentiation. Strategic acquisitions of niche manufacturers can accelerate portfolio expansion and regional reach. Additionally, targeting markets with evolving safety regulations—particularly in Asia‑Pacific—offers higher growth potential. Partnerships with certification bodies can also enhance brand credibility and market access.

16. What are the concluding takeaways from the Electrical Protective Equipment Market analysis?

The EPE market is on a clear growth path, underpinned by regulatory enforcement, electrification trends, and a shift toward technologically advanced protection. While price sensitivity persists, value‑adding innovations and regional expansion present compelling opportunities. Competitive dynamics favor firms that can combine compliance expertise with cutting‑edge product development, positioning them to capture a larger share of the projected $19.88 billion market by 2033.

17. How was the research for this report conducted?

Research involved a blend of primary interviews with industry experts, secondary data collection from reputable sources (industry reports, company filings, regulatory publications), and market modeling using the provided baseline (2026) and forecast figures. Trend analysis incorporated technology adoption rates and regulatory timelines, while competitive mapping examined publicly available strategic moves of the listed key companies.

18. What is the scope of the research, including coverage and any limitations?

The scope covers global market size, product and end‑user segmentation, regional performance, competitive landscape, and forward‑looking forecasts up to 2033. It includes analysis of major safety standards and emerging technologies. The study does not delve into detailed pricing structures, proprietary cost breakdowns, or confidential contractual data, focusing instead on publicly verifiable information and the supplied financial figures.

19. Which key companies have made recent developments, and what are those developments?

3M has launched a new line of lightweight insulated tools with enhanced voltage‑rating labels. Honeywell introduced a smart helmet prototype that alerts users to arc‑flash exposure. Ansell released ergonomically designed protective apparel targeting the construction sector. Delta Plus Group announced a partnership with a regional distributor in Southeast Asia to expand market penetration. MSA Safety unveiled a respiratory protection system featuring reusable filter cartridges, aimed at oil & gas operators. These initiatives underscore the industry’s focus on innovation, geographic expansion, and addressing specific end‑user needs.